I just received a letter that my policy will not be renewed when it expires in October. I’m currently with ISU Westlake. This is a huge blow.

Looks like I’ll be reaching out to Amanda from @Swood as well.

I just received a letter that my policy will not be renewed when it expires in October. I’m currently with ISU Westlake. This is a huge blow.

Looks like I’ll be reaching out to Amanda from @Swood as well.

Dang, I better get discount with all the business I’m sending their way!

Updating this thread: Amanda was kind enough to reach out to @liberationfab and me to see how she could help out the builders. Amanda complied a flyer with some info and services. I know this information will be very useful to the aspiring framebuilder or lurker.

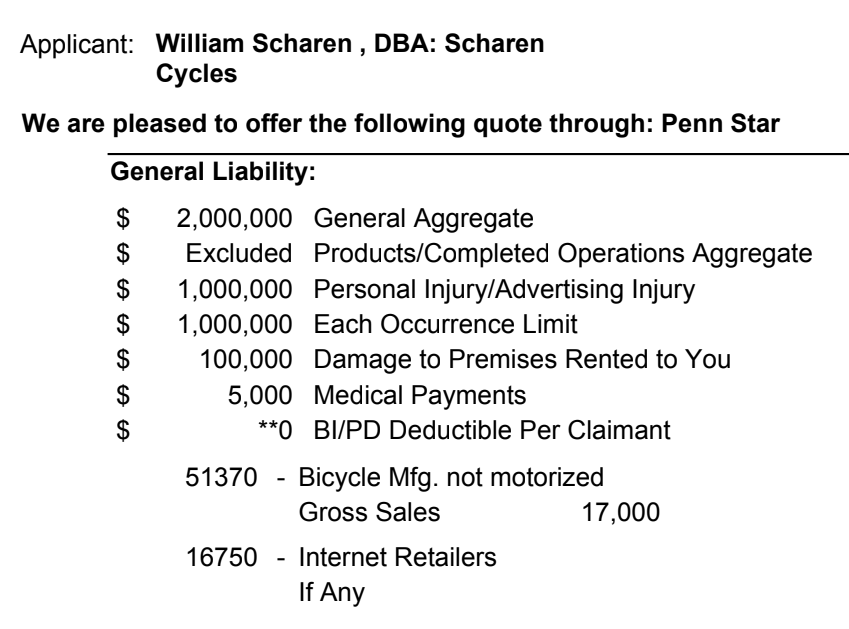

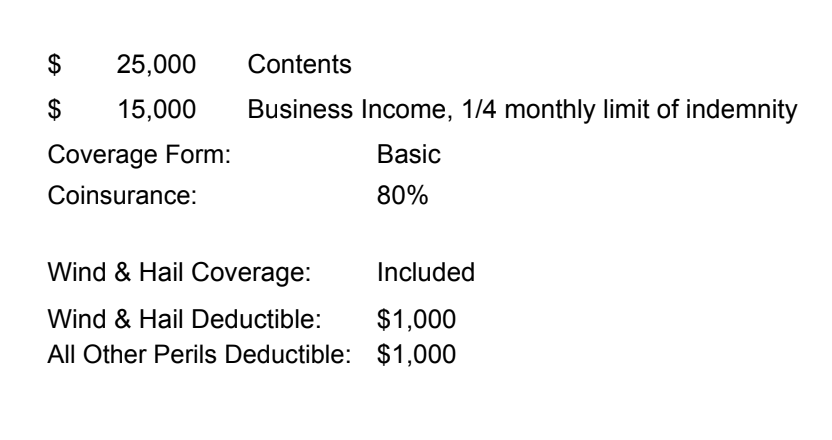

Insurance MMA.pdf (586.0 KB)

Hello my name is Amanda Gearheart, I am an Insurance Placement Specialist with Marsh & McLennan Agency aka MMA. I have helped place insurance coverage for numerous custom frame and bicycle part fabricators. My team primarily focuses on Small Business accounts for Sole Proprietors, Corporations, LLC’s, etc. in all industries domiciled in the United States.

There have been several questions posted regarding insurance lately and to help educate Fabricators here are some general insurance terms along with a brief description.

General Liability also known as Business Liability - protects insured’s from suits brought by a third party claiming, bodily injury, and property damage or financial loss. General Liability can also include Products Liability, this can protect fabricator, manufacturers, distributors, suppliers, retailers, and others who make products available to the public and are held responsible for the injuries those products cause. For Foreign sales, coverage would only apply if claims are filed in the U.S.

Property and Tools - Coverage for Buildings, Business Personal Property and Tools, Stock & Inventory

Workers Compensation - Requirements vary by state- Workers’ Compensation: State by State Guide

Excess Liability - Higher excess limits over General Liability, Employers Liability and Auto Liability.

Hired and Non Owned - If an employee of your company is driving to a work-related event in their personal vehicle or a rented car and has an accident.

Auto – Liability and Physical Damage.

To obtain a quote for coverage, we will require a completed application and any additional information depending on your insurance needs. If you are interested, please reach out to me directly.

I was able to get finally get a quote from Westlake and it was huge. I reached out to Amanda at MMA and it was awesome! Same coverages and a helluva lot less. Thanks @Swood!

This is great info! Whomever is quoting the new 2-3X insurance cost seems quite predatorial as they didn’t provide a quote until 3 days before my policy expired… surprise! Let’s hope for better from MMA.

I contacted Amanda to get a policy and she was very helpful and set me up. It was going to cost about $1850 a year. Before the policy went active I was contacted by a local rider in my area who wanted me to build him a bike and also happened to be an insurance broker with Valor. He just got me a policy with better coverage for $930 a year.

Ricardo Nuñoz

rnunez@valoragent.com

Is there a specific annual volume or revenue associated with that number?

Insurance rates will always be based on annual revenue, annual units sold, or a combination of both. Rates can also vary depending what you make and sell based on an insurers assessment of risk. Everyone should read their policy front to back to make sure they not only understand their coverage but to make sure you are actually covered for what you are selling and what you are making. Don’t understate your sales or withhold information about what you do, lawyers are more predatory than insurance companies.

Yes, I understand the basics. Liability insurance for my skills coaching and event biz is the same. I’m more trying to get a frame of reference for the numbers people are posting here.

Is this for 10 units or 50 units annual? Just posting a dollar amount on here without any other frame of reference doesn’t really tell us anything.

My response wasn’t intended as a reply directly to you, it was a blanket statement to support your question and help others understand the wide variance in insurance options and prices for similar products and services.

For reference, I pay about 950usd/yr for product & general liability (2 million) up to 250k annual revenue. I went through a local (Portland, OR) broker and the policy is with Markel/Evanston insurance company. Took some work to find an insurer that understood small-time manufacturing. They have a description of each product I make and my installation instructions on file, which I can update at any time to add new products. Premium is based on overall revenue, so plenty of room to grow – I’m nowhere near 250k.

As a sidenote, it’s my understanding that forming an LLC doesn’t do anything to protect you from personal liability unless your business has significant assets.

Thanks for the info! that is more reasonable than I expected to be honest.

My small bike instructing biz is around $900 annual for general liability up to $3 million and that is the cheapest option based on number of clients (up to 50). Definitely not gonna hit $250k revenue with that!

I was expecting general liability for manufacturing to be in the several thousands.

I quoted an annual projected revenue of $50K for my bike biz (it will likely be lower than that but I didn’t want to over state it) The rate he got me may have been low because I also moved my insurance for my other business (photography) to him as well. I really don’t know, but Ricardo could give you more details. He saved me a ton of money on that photo biz policy from my previous insurer, Hiscox, and both policies have the same or better coverage than I previously had.

My policy with ISU Marvin recently expired and the new quote was 40% higher than what I was paying before ($2,450 from $1,750). This is quite a hit for me, as I’m not getting any orders lately and the money is all coming out of income from my day job. I still may go back to them, but am reaching out to Amanda at MMA to see what I get there.

I tried to get coverage through my local Allstate agency and was temporarily very excited to get a quote for a little over $900. However, the general liability policy they were offering left a gaping hole in one of the most important places: products/completed operations. This is part that covers your product after it leaves your hands. I share this as a heads up to others who are trying to get low-cost coverage.

I can’t “heart” this post. Wow, what a jump in cost!

Amanda at MMA came through for me with a policy through Berkley Aspire. It took no time to get approval compared to what I’m used to - and the price is great! $1,650 annually for a projected $15,000 in sales. That’s $100 less than the policy I had last year and $800 less than my quote for this year from the old company. I’m pleased. Seems the way to go for low-production builders here in the US at least. If I magically start selling more frames that may change, but I’m not holding my breath.

Mine is up for renewal and went up to $2300/yr… I gotta investigate and figure out why that happened.

my policy with MMA just renewed with a similar rise. i asked about the price increase and was told it’s happening all over and it’s still a good deal. ( but in nicer wording)

Does anyone have an updated contact for Amanda at MMA?

I had sent an email last week about quoting a general policy with no response.

Tried to call the phone number in the PDF - but got a dead number message from Verizon.

Anyone know of any other decent options that understand small framebuilders?

My account got transferred to Jamie, it might be worth reaching out to them: Jamie.Frazier@marshmma.com