Thank you! I’ll reach out to them!

Hello everyone! It has been brought to my attention that a few shops were unable to get through to me for insurance inquiries, so I wanted to confirm, my contact information has remained the same. My email is Amanda.Gearheart@MarshMMA.com and my direct phone number is 336-878-7839. We have a new market that has opened up for Bicycle Fabrication that we are quoting with now as Berkley Specialty is increasing their minimum premium. For all of you that are currently with Berkley Specialty, we will remarket at your renewal. The new insurance company is offering the minimum premium at $1,500 annually plus tax and fees for General Liability coverage to include products and completed ops. Please feel free to reach out if you should have any questions. Thank you!

11 Likes

We just renewed our policy, the good folks over at MMA found us a new provider, Mesa Underwriters Specialty Ins Co.

Total annual premium for 50k expected revenue is $1687. Not bad!

3 Likes

If I were to build frames for one year, pay for coverage, and then quit, how long would I have to carry said coverage for it to remain applicable to that year of production and sales?

The common wisdom is that you keep the insurance until all units are no longer in use.

1 Like

I’d say that’s a fairly good approach. I know in Australia there is at least a 10 year (might actually be 12 year) statute of limitations on liability for consumer products. So if I was building here, or selling bikes as I currently do, I’d budget to have insurance for at least a decade after business is wound up (or if I’m lucky enough to retire). The retirement one is a big one to consider as 10 years of insurance payments could become a sizable cost.

4 Likes

I’m grateful to this thread (thank you all!), which helped me secure insurance with MMA, Ryan Turner Specialty, and Mesa Underwriters Specialty Insurance Co. I did have some challenges, which I want to share in case it helps others, but hopefully it’s just me. MMA did resolve everything for me.

1. Verify your policy number with MMA. I was assigned two policy numbers, and later learned the first was only for the quote, despite it appearing on my first payment portal.

2. Verify you’re receiving invoices by email. I made my second payment using the same portal as the first, which led to confusion, temporary cancellation of my policy, and missing funds, later resolved.

3. Verify you have your policy on file. I mistook the first document sent to me as the policy, with page titles like “Confirmation of Insurance” and “Insurance Binder.” My policy, which I subsequently requested, has a signed “Commercial Insurance Policy” page.

I believe the key issue was that Ryan Turner/Mesa did not have my email address on file, so wasn’t communicating with me.

1 Like

I’m a super low-volume hobbyist (only 2 frames last year, less than 10 likely this year) trying to figure out the smart way to be able to safely make frames for friends, acquaintances, etc. From everything I’ve read both here and elsewhere, even if you’re making frames “at cost”, the liability picture in the USA doesn’t really change compared to straight up sales. Basically, if you’re making frames for people where you’re getting any kind of compensation (even them buying the parts), you’re liable.

I’m willing to accept this as fair, but the cheapest quote i’ve gotten at my volumes is $1750/yr, and while that’s in the range of what I’d be willing to spend if I manage to make ~10 frames, it starts to get a little crazy just to stick my neck out and see if this whole framebuilding thing works. I’m looking to be clever, and wondering if anyone else has some hard-won wisdom they’d be willing to bestow. A few options i’m currently considering:

- Partner with my local bike shop who I have a great relationship with. Work as a contractor for them building bikes under my brand, they add product liability to their policy in exchange for them being my “official” dealer for bike fits, builds, and continuing maintenance. Seems like a good deal for me, but going to add unnecessary overhead to everyone’s bikes at this scale, and I worry about the lack of control from my end.

- Partner with another local framebuilder who has insurance, and do business within his LLC under my brand. Unsure how this will work in practice- perhaps we can split the total cost of liability and save money if we operate as one?

- Find some kind of personal liability/umbrella coverage that would cover me as an individual human making frames for fun at cost, that means someone cant crash 5 years from now and clean my life savings out.

Happy to hear anyone’s thoughts, even if they’re “suck it up and pay the $1750, you dolt”.

3 Likes

I have insurance through Mesa Underwriters Specialty Insurance company and it is less than half the yearly cost you mentioned.

Maybe you can get an independent agent to check with them. I am certainly not the only frame builder using them

2 Likes

Unfortunately this is an expense you have to bear if you want your ’customers’ and yourself protected. You also have to make sure you are covered properly…….because the underwriters delved deeper into what I was doing they upped my premiums as they didn’t realise I used a flame and melt metal. I did explain that to them right at the start a few years ago but they didn’t pick up on it, which is a concern to be honest. I am now at Aus$3300 a year and given the last 12 months have only seen two orders that’s over $1500 per frame, which obviously I have to carry myself as the amortising was worked out on 6-10 frames…….sort of.

1 Like

It might be a LOT more than that, if you retire next year but have to keep paying for the insurance… forever? I ain’t no lawyer but I think your liability doesn’t go away if you close up shop. It might be cheaper to buy back all the frames you sold, than to keep paying the insurance.

Anyone here set up an LLC or some such that can go out of business and not exist anymore, and thus escape liability? Or can they still go after the owner of the defunct LLC? I’m sure it varies by country.

Don’t worry, I’m not literally asking an internet forum on bike frames for free legal advice. Just making conversation.

2 Likes

Yeah I need to do some research on that. I think the laws here in Australia are different but can’t say for certain I need to continue the cover. I’ve so far read two different ideas on that.

Great question. Worth setting up a company I think. Couldn’t you also get people to sign something saying they agree you have no liability for injury etc.? Whenever I’ve bought a regular bike from a shop there’s a disclaimer about that.

1 Like

I absolutely could, and WILL, but from my initial research it seems that those types of waivers (in the US) aren’t worth much more than the paper they’re printed on. It would certainly bolster my protection in a scenario where I do have explicit product liability, but doesn’t seem to even come close to enough to protect on its own.

I took a leap and reached out to the local shop last night, and happily they were very interested. It’ll come down to how much their insurance would go up vs what I could get to cover on my own, and whether the increased cost to them is worth it for the additional business/marketing I could bring them. Everything I do is custom geo, and one of their primary revenue streams is bike fitting, so hopefully there’s some good synergy there.

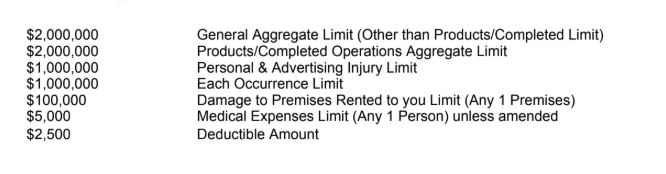

@Restless really appreciate that additional datapoint and I will certainly be reaching out to them! Less than half could easily turn this from a blocker of a cost to something fully feasible. Would you be willing to share your agent’s contact? The quote I’m referring to is from Mesa Underwriters so maybe I’m just asking for the wrong thing. Here’s the coverage they quoted:

1 Like

That sounds like a great way to get some leads for projects as well!

I’m surprised at the amount of the coverage. Here my policy is $20million product liability and 20m personal as well as fire etc.

My agent:

Tom Wilson

Ashland Insurance, Inc

PO Box 880

585 A St. Suite #1

Ashland, OR

97520

541-608-1870 direct

541-482-0831

541-488-5851 fax

twilson@ashlandinsurance.com

California Agency License # 0807521

1 Like

Just to close the loop on this convo for who may be interested now or in the future, I did call and speak to Tom to discuss his rates. The output of that call is that Mesa Underwriters’ policy minimum has gone up in recent years, so there’s no real practical way to get the rates down below $1500 currently. Worth knowing as a datapoint for anyone in a similar position to me who wants to take the leap but is trying to figure out what volume would justify it.

2 Likes

What kind of business structure is the best option. Sole proprietorship, LLC, etc?

Depends on what you’re comfortable with and often how big you are. If I remember correctly, in the U.S. a sole proprietorship business is not separated from the owner; in fact, even if you have a business name and EIN, in the eyes of the IRS your business is still just you and your name. This is where the “doing business as” comes in (often just shortened to “DBA”). You and your finances have no protection in a sole proprietorship, as it’s all under your name.

LLC, on the other hand, is regarded as a separate entity from the owner, so provides some legal protection to you in case of a lawsuit. How much though, I’m not sure… It’s probably very situationally dependent (property damage vs injury, how ambitious is the lawyer, etc…) My experience is only with a sole proprietorship (as a small janitorial company and a low-voltage contractor) with liability insurance for protection. …For those wondering, around $900 a year for a $2 million limit.